On February 7, Hurupay confirmed that its public token sale had officially closed without reaching its $3 million minimum raise. The company announced that it would process refunds and return funds to participants shortly. The announcement ended weeks of debate across crypto social channels and effectively marked another high-profile failure for the ICO model in its present state.

Hurupay entered the market with metrics that, in prior cycles, would likely have guaranteed funding. The team brought revenue, users, institutional partnerships, and a working product. None of that proved sufficient in current conditions.

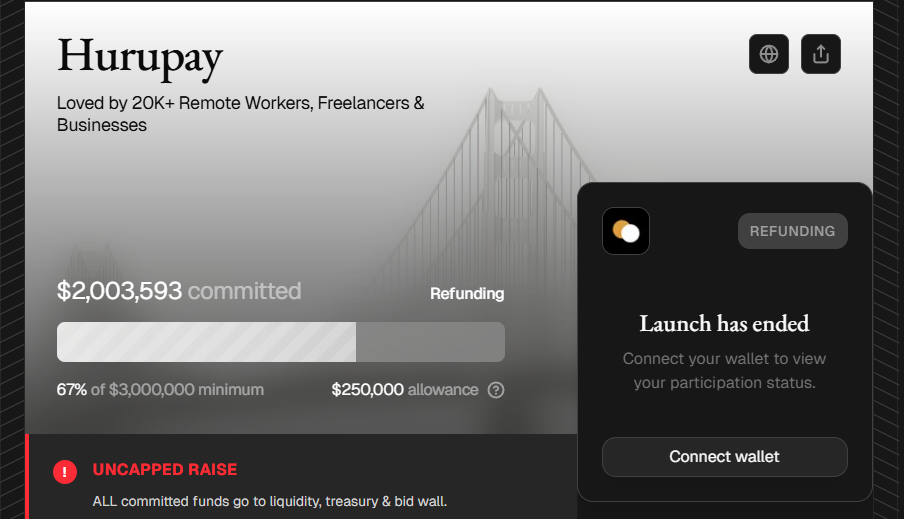

The Hurupay ICO and Outcome

Onchain neobank Hurupay launched its ICO on MetaDAO with a minimum target of $3 million and an ideal raise of $5 million or more. The sale used an uncapped structure aiming to prevent gaming and to allow market pricing to emerge naturally. All contributed funds would flow directly to the Hurupay treasury if the minimum threshold was met.

Despite steady participation, the raise never approached the required level. In the final minutes, a single participant apparently committed $1.1 million, pushing total commitments past $2 million and briefly creating confusion as related prediction markets resolved to a successful outcome.

The commitment still fell short of the stated minimum. Hurupay closed the sale and confirmed refunds for all contributors.

The company’s public statement remained concise and factual. It thanked participants and reiterated that the minimum threshold had not been met. Several observers noted that failing to raise the minimum amount even after deciding to change the mechanics of the sale midway set an important precedent for maintaining credibility in onchain fundraising.

Leading up to the sale, Hurupay published detailed operating metrics. Over the prior six months, the company increased monthly transaction volume from approximately $1.8 million to $7.2 million, compounding at a 32% month over month growth rate. Over twelve months, Hurupay processed more than $36 million in total volume and generated over $500,000 in revenue.

Individuals and remote workers use Hurupay to receive USD, convert to stablecoins, and spend or withdraw locally. Businesses use the platform to run recurring global payroll and supplier payments without requiring U.S. incorporation or local banking infrastructure. The company counts more than 30,000 users across Asia, Africa, Europe, and the United States. None of these factors translated into sufficient retail capital during the ICO.

MetaDAO Mechanics & Overflow Refunds

The sale exposed growing friction around MetaDAO’s evolving ICO mechanics. Earlier launches returned excess capital to participants, which created a perception of downside protection and encouraged participation tied to prediction market strategies. Hurupay’s sale removed overflow refunds and directed all funds to the project treasury once the minimum was met.

Critics argued that the change altered the risk profile for retail participants and favored last-minute capital deployment. MetaDAO’s co-founder, Metaproph3t, countered that uncapped raises reduced manipulation and better reflected genuine demand.

He publicly acknowledged that the team continues to iterate on the model and that Hurupay suffered from poor timing in a weak market.

Market conditions and eroding confidence

The Hurupay outcome followed several troubled ICOs, including Ranger Finance and Trove Markets, and Space, each of which struggled to meet post-sale expectations. Ranger Finance and Trove Markets traded significantly below their ICO prices after launch, while Space faced scrutiny over its $20 million raise and questions around valuation, disclosure, and post-ICO accountability. Together, these outcomes eroded trust in new token sales, particularly among retail participants who bore most of the downside risk.

Multiple commentators noted that large participants from previous MetaDAO launches did not meaningfully engage in the Hurupay sale, attributing earlier successes to arbitrage around prediction markets rather than long-term conviction.

Others pointed to weak marketing, lack of narrative momentum, and the absence of Solana-native appeal as contributing factors.

Hurupay did not fail to ICO because it lacked a product, revenue, or users. It failed because the ICO model no longer aligns with current market psychology and because the onchain neobank space has become increasingly overcrowded, with even MetaDAO having hosted at least one similar project in the past. Market participants now face a landscape where nearly every crypto wallet positions itself as a global banking alternative, compressing differentiation and raising the bar for attention, with Jupiter’s launch of Jupiter Global being a recent example.

Retail investors demand liquidity, clarity, and immediate feedback. ICOs ask for patience, trust, and long-term horizons at a moment when capital remains risk-averse and fatigued. In this environment, even credible operators struggle to stand out.

Read More on SolanaFloor

Solana Co-Founder Anatoly Yakovenko Shares Vibe-Coded Percolator Memecoin Perps as Developers Fork the Project

Is the Crypto Crash Over, Or Will the Unwind of DATs be the Final Capitulation Event?

Are You Participating in Solana Seeker Season 2?