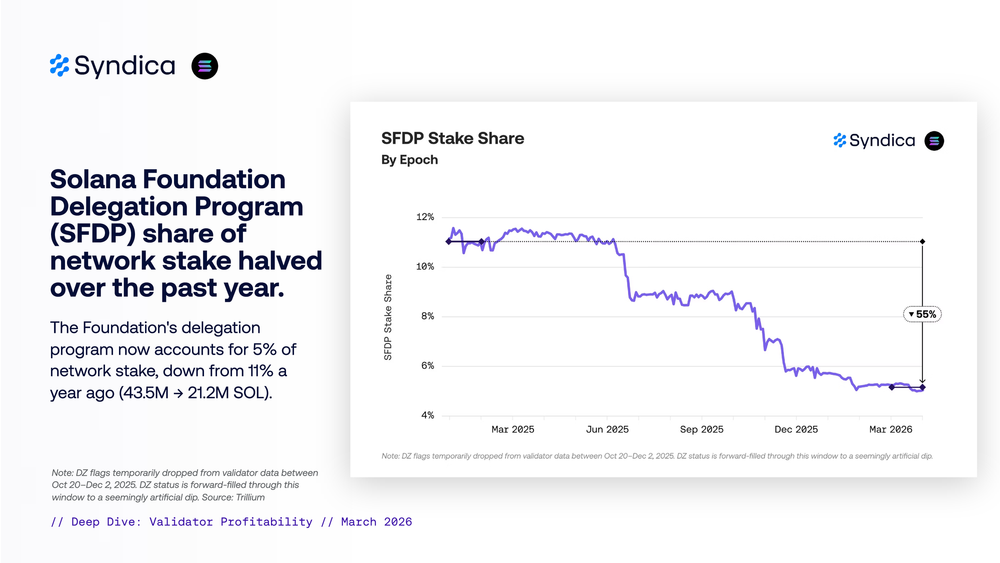

L'ultimo approfondimento di Syndica sull'attività onchain di Solana evidenzia una forte riduzione del ruolo del Programma di Delegazione della Fondazione Solana nella rete. Nell'ultimo anno, la quota di partecipazione totale del programma è scesa dall'11% al 5%, passando da 43,5 milioni di $SOL a 21,2 milioni di $SOL.

Questo cambiamento riflette una strategia deliberata. La Fondazione Solana ha introdotto il programma di delega nel novembre 2020 per favorire l'avvio della partecipazione dei validatori durante la fase iniziale della rete. All'epoca, i costi operativi elevati e la delega limitata da parte di terzi creavano ostacoli per i nuovi validatori. Il programma ha affrontato questa lacuna delegando la partecipazione a operatori più piccoli in base alle prestazioni.

Con la maturazione dell'ecosistema, la delega esterna si è espansa in modo significativo. Dal lancio, le quote di partecipazione non appartenenti alla Fondazione sono cresciute di circa il 230%, mentre le quote totali delegate sono aumentate di circa il 95%. Nell'aprile del 2024 la Fondazione ha modificato il proprio approccio per dare priorità all'indipendenza dei validatori piuttosto che al loro numero totale.

Più di recente, la Fondazione ha ridotto attivamente la propria impronta attraverso cambiamenti di politica volti ad accelerare l'indipendenza dei validatori. In base a una nuova regola, per ogni nuovo validatore aggiunto al programma, tre validatori vengono rimossi se detengono quote della Fondazione da più di 18 mesi e mantengono meno di 1.000 $SOL in quote esterne. Questo approccio spinge i validatori ad attirare la delega della comunità, riduce la dipendenza a lungo termine dal sostegno della Fondazione e rafforza un insieme di validatori più efficiente e decentralizzato.

I risultati mostrano ora un insieme di validatori più piccolo ma più autosufficiente. I validatori che detengono almeno 50.000 $SOL al di fuori del supporto della Fondazione sono aumentati del 121% da aprile 2024. Allo stesso tempo, il numero di validatori supportati dal programma è diminuito del 59%, rispetto al calo dell'8% dei validatori non supportati.

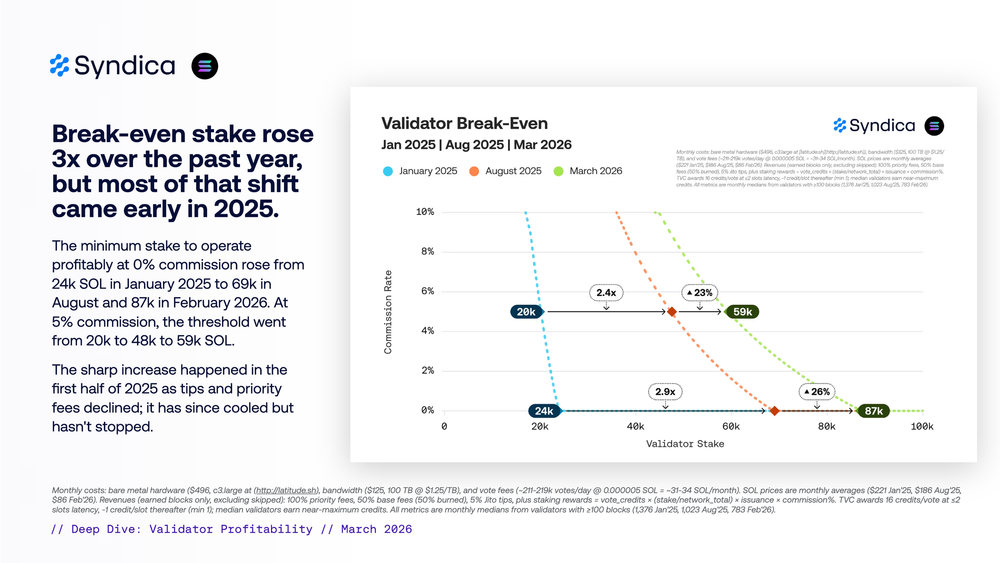

L'economia dei validatori si restringe con l'innalzamento della soglia di break-even

La redditività dei validatori è diventata più impegnativa. La puntata minima richiesta per raggiungere il pareggio è aumentata notevolmente nell'ultimo anno, soprattutto nei primi mesi del 2025.

Con una commissione dello 0%, la soglia di pareggio è passata da 24.000 $SOL nel gennaio 2025 a 69.000 $SOL in agosto e a 87.000 $SOL nel febbraio 2026. Con una commissione del 5%, la soglia è passata da 20.000 $SOL a 48.000 $SOL e poi a 59.000 $SOL.

La maggior parte di questo aumento si è verificato nella prima metà del 2025, a causa del calo delle mance e delle commissioni di priorità. Sebbene il ritmo di aumento sia rallentato, i costi rimangono elevati. Questa tendenza è in linea con le preoccupazioni più ampie dell'ecosistema, secondo cui i validatori più piccoli stanno affrontando una crescente pressione finanziaria.

Anche la struttura dell'insieme dei validatori è cambiata. All'inizio del 2025, la distribuzione degli stake mostrava una lunga coda di validatori più piccoli. A marzo 2026, questa coda era in gran parte scomparsa. La maggior parte dei convalidatori opera ora in una fascia compresa tra 100.000 e 1 milione di $SOL, creando una distribuzione più pesante. La concentrazione di stake tra i top validator è rimasta sostanzialmente invariata.

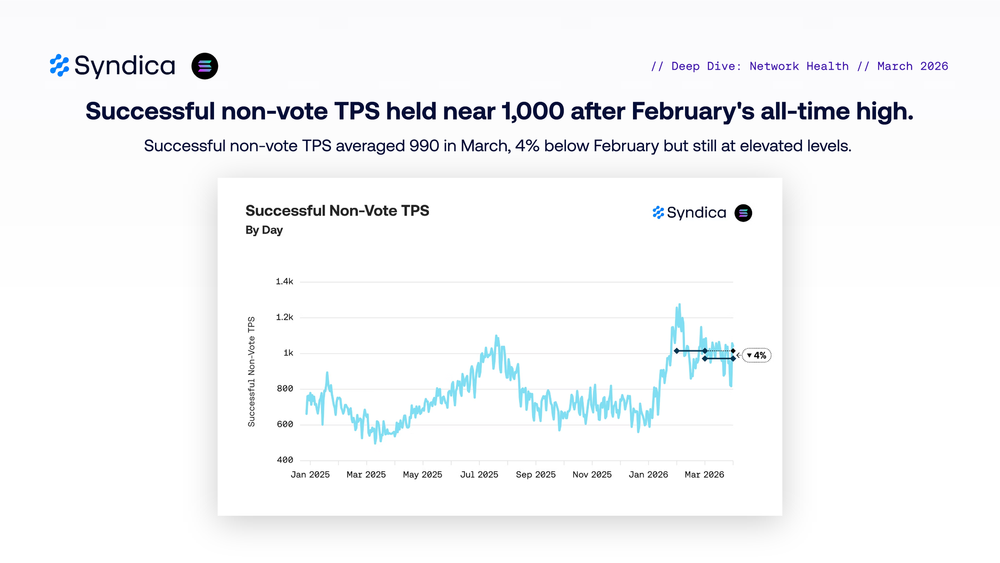

Le prestazioni della rete si mantengono vicino ai livelli massimi

Nonostante i cambiamenti nella composizione dei validatori, le prestazioni della rete rimangono elevate. Le transazioni non di voto riuscite al secondo sono state in media 990 a marzo, solo il 4% in meno rispetto al massimo storico di febbraio e ancora vicine ai 1.000 TPS.

L'efficienza del voto è leggermente diminuita, ma rimane elevata. Circa il 94,5% dei voti si colloca all'interno di uno slot, in calo rispetto al 97,8% di dicembre. Tuttavia, il 99,3% dei voti si colloca ancora entro due slot, il che indica un'affidabilità costante. La latenza dei voti è aumentata modestamente a 1,08 slot, con un incremento di circa il 5% rispetto alla precedente linea di base. I tassi di successo delle votazioni rimangono superiori al 99,7%, con poche variazioni rispetto all'anno precedente.

La domanda di calcolo si è raffreddata a livello mediano, con un calo dell'8% mese su mese delle unità di calcolo mediane per blocco. Tuttavia, la domanda di picco rimane forte. I blocchi ad alto percentile continuano ad avvicinarsi al limite di 60 milioni di unità di calcolo.

La diversità dei clienti del Validator si espande

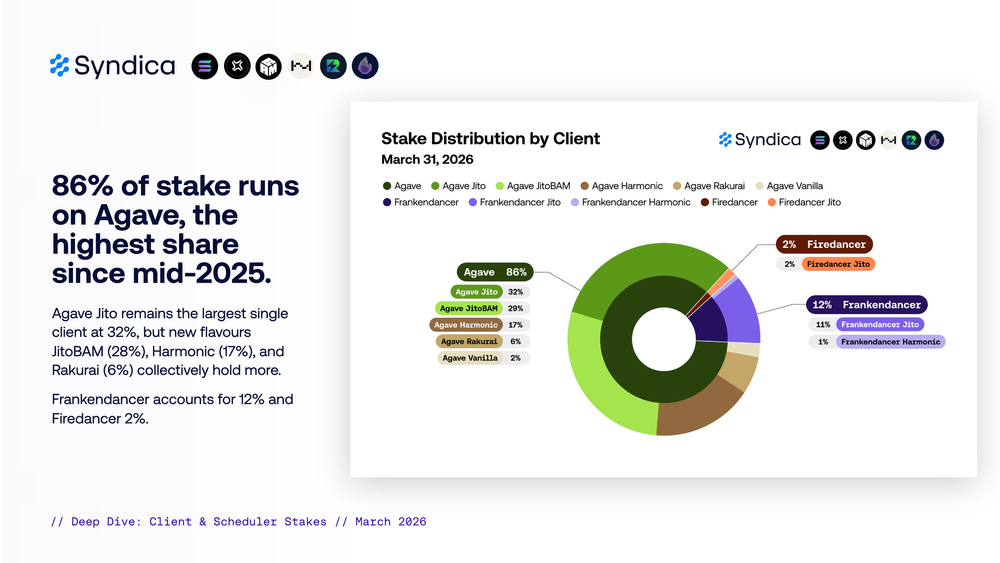

I dati sulla distribuzione dei clienti mostrano sia la concentrazione che la diversificazione. Agave supporta ora l'86% della partecipazione totale, segnando la quota più alta dalla metà del 2025.

All'interno di questo ecosistema, Agave Jito rappresenta il 32% della quota. Tuttavia, le varianti più recenti del cliente superano collettivamente tale quota. JitoBAM detiene il 28%, Harmonic il 17% e Rakurai il 6%. Frankendancer rappresenta il 12%, mentre Firedancer il 2%.

L'utilizzo degli scheduler è equamente suddiviso. Gli scheduler Balanced e Revenue Optimized controllano ciascuno il 47% della partecipazione, mentre la quota restante è distribuita tra configurazioni più piccole.

Comunità a favore di una maggiore decentralizzazione

I dati indicano una rete che si sta evolvendo verso un numero minore di validatori, ma economicamente più indipendenti, e il cambiamento ha suscitato reazioni in tutta la comunità. Il cofondatore di Solana , Anatoly Yakovenko, ha commentato il cambiamento con un'osservazione ironica, definendo il SFDP "l'unico programma governativo che sia mai stato tagliato".

Max Kaplan, Chief Technology Officer di SOL Strategies, ha contestato direttamente la tesi secondo cui Solana dipende dalla Fondazione per la sua sopravvivenza.

Questa reazione si inserisce in una critica di lunga data, secondo cui il set di validatori di Solana si basava pesantemente sulla delega della Fondazione, sollevando preoccupazioni sulla centralizzazione. La massiccia riduzione della partecipazione alla SFDP nel corso del tempo sfida direttamente questa tesi.

Disclaimer: SolanaFloor è di proprietà e gestito da Jito Foundation.

Per saperne di più su SolanaFloor

La società Solana segnala il ritorno all'accumulo di $SOL con un aumento di 8 milioni di dollari

$BNSOL rivendica la corona LST di Solana in mezzo alla fuga dei depositi DeFi

Qual è la più grande minaccia per la DeFi nel 2026?