Solana Aggregator Wars: An In-Depth Look at Volume Share, DEX Routing, and Private AMMs

Aggregators Dominate: Over 50% of Solana’s Monthly DEX Volume

- Published:

- Edited:

Despite recent signs of cooling enthusiasm in decentralized exchanges (DEXs), the competition among aggregators on Solana remains fierce, signaling their critical role within the ecosystem. Aggregators have not only maintained substantial monthly trading volumes but also solidified their dominance as key infrastructural components of Solana’s trading landscape.

Aggregators Claim the Lion’s Share

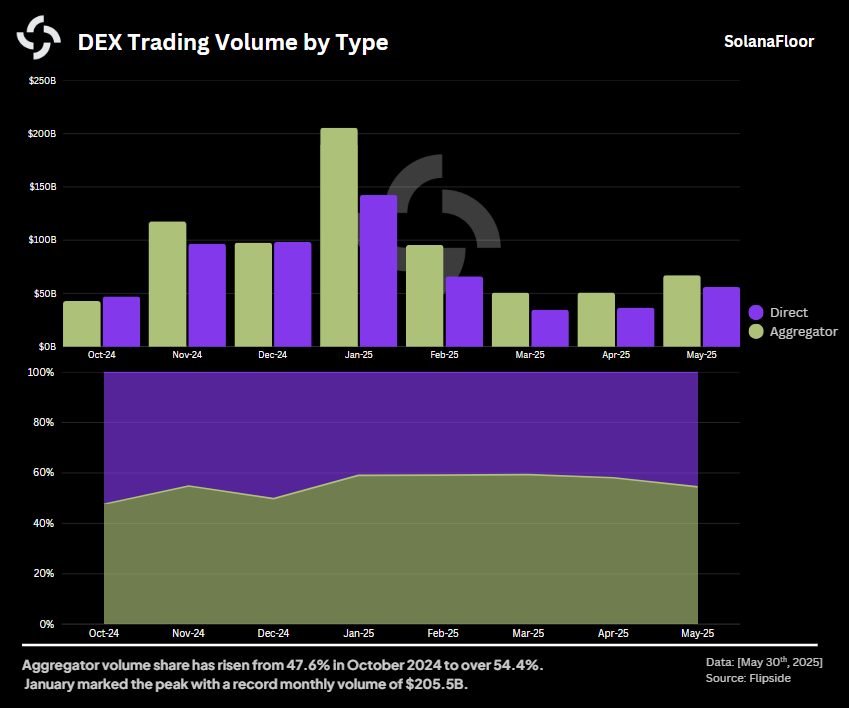

Based on Flipside, onchain data highlights the pivotal position aggregators occupy. Over the past eight months, aggregators have consistently accounted for between 47.6% and 59.3% of total monthly DEX trading volume. This sustained dominance was particularly pronounced in January 2025, when aggregators collectively processed an all-time high of over $205 billion in monthly volume.

Based on Flipside, onchain data highlights the pivotal position aggregators occupy. Over the past eight months, aggregators have consistently accounted for between 47.6% and 59.3% of total monthly DEX trading volume. This sustained dominance was particularly pronounced in January 2025, when aggregators collectively processed an all-time high of over $205 billion in monthly volume.

Since December 2024, aggregators have consistently handled more than half of all DEX trading activity on Solana, showcasing their strategic importance even amidst the market fluctuations tied to memecoin volatility. Although trading volumes have cooled from their January peaks, activity surged again in May 2025, hitting $67 billion, representing a substantial 31.8% increase compared to the previous month.

Jupiter: The Undisputed Leader

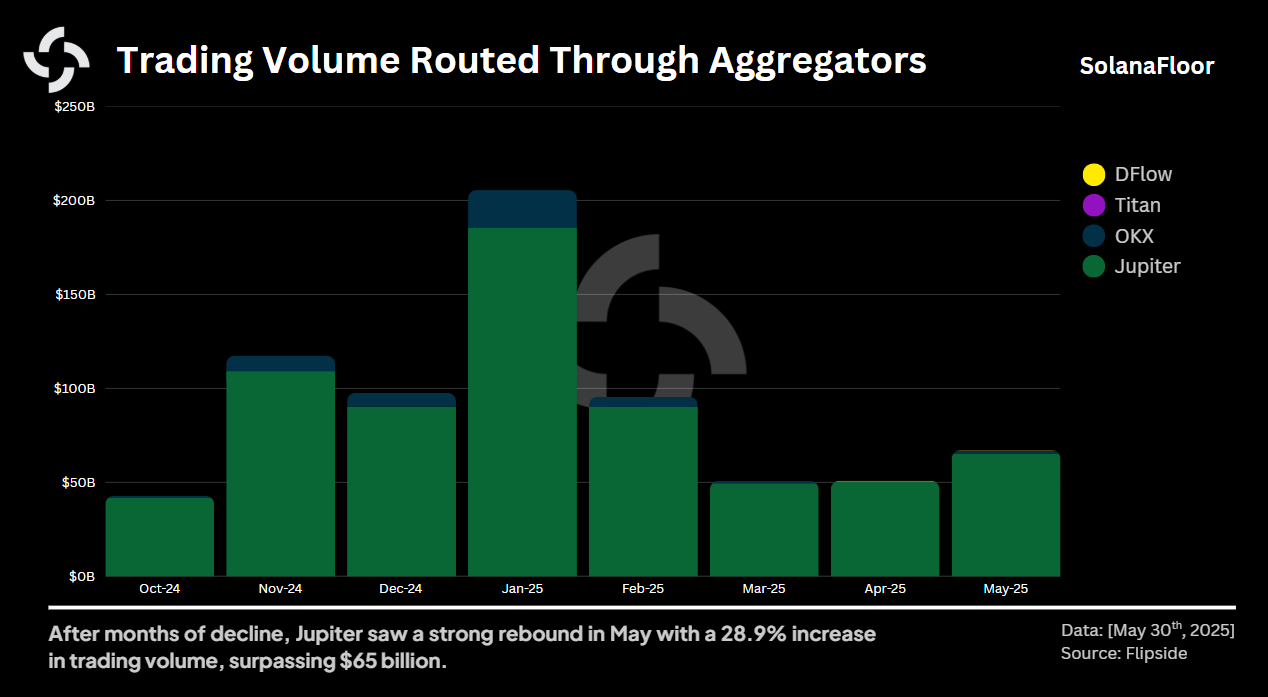

Amidst intense competition, Jupiter has maintained a clear lead, handling the vast majority of aggregator volume on Solana. In January alone, Jupiter processed trades amounting to a staggering $185 billion. Competitors like OKX have also captured attention, notably hitting their own peak of $20.1 billion in trading volume during the same period.

Amidst intense competition, Jupiter has maintained a clear lead, handling the vast majority of aggregator volume on Solana. In January alone, Jupiter processed trades amounting to a staggering $185 billion. Competitors like OKX have also captured attention, notably hitting their own peak of $20.1 billion in trading volume during the same period.

Emerging players Titan and DFlow, while still in the early stages of growth, have shown promising momentum. Titan reached $55 million in trading volume by May, while DFlow saw volumes of $182 million, signaling the potential for increased competitive pressure in the coming months.

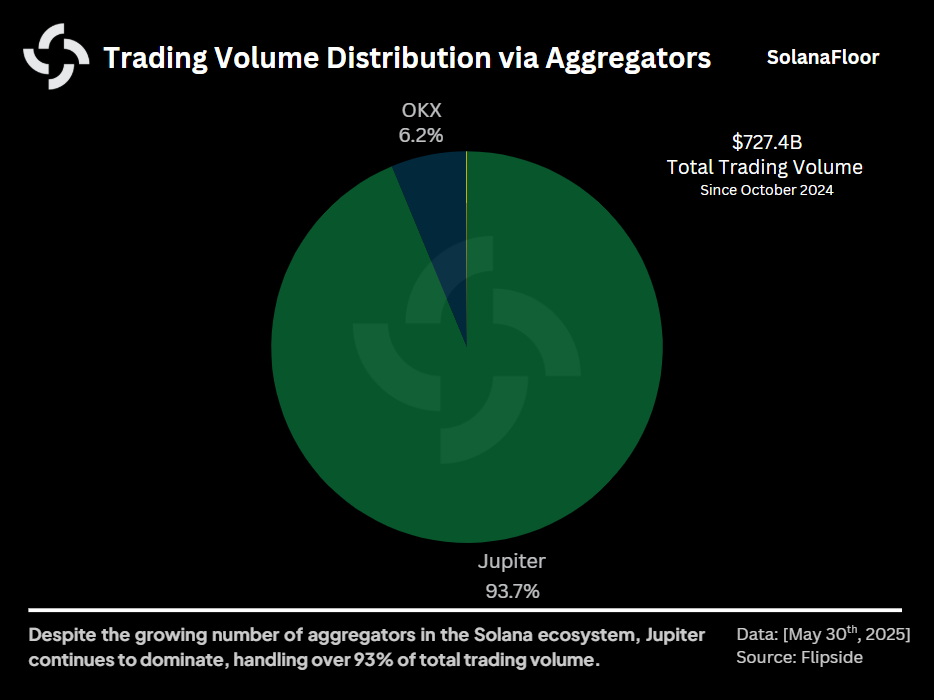

However, looking at the broader picture of the past eight months, Jupiter overwhelmingly dominates, responsible for over 93.7% of the total aggregator volume ($727 billion). OKX follows distantly at 6.2%, while Titan and DFlow collectively represent less than 0.1% of total volumes.

However, looking at the broader picture of the past eight months, Jupiter overwhelmingly dominates, responsible for over 93.7% of the total aggregator volume ($727 billion). OKX follows distantly at 6.2%, while Titan and DFlow collectively represent less than 0.1% of total volumes.

Diverging Strategies and DEX Diversity

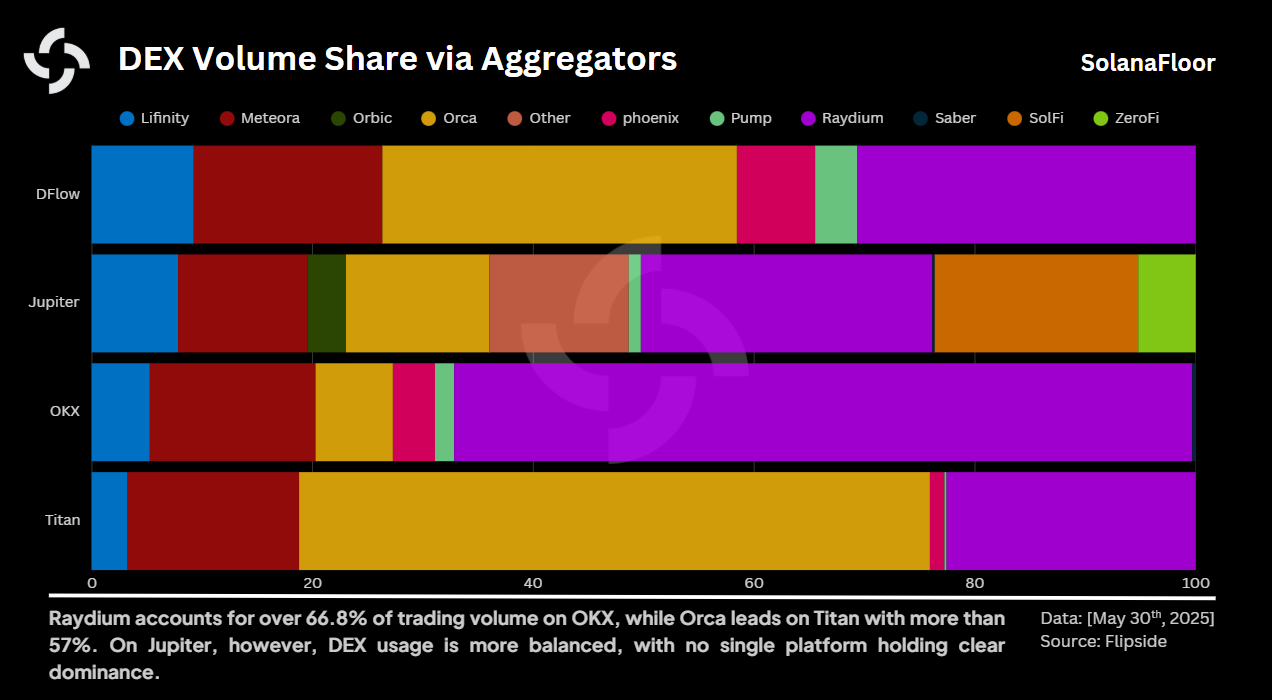

Each aggregator adopts a distinct strategy in selecting decentralized exchanges for trade routing, reflected in the varying degrees of diversity among them.

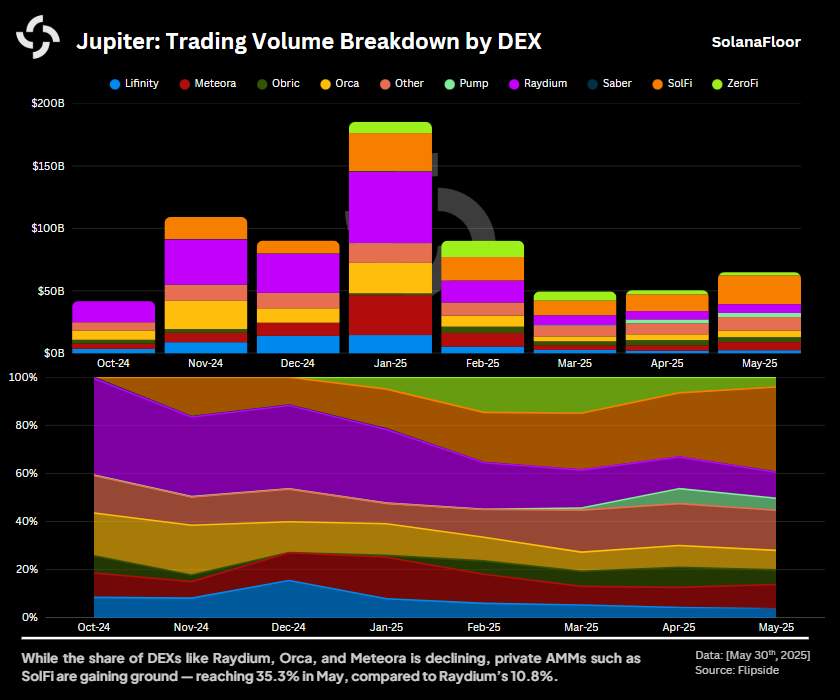

Jupiter notably excels with its highly diversified portfolio of DEX integrations. Within Jupiter’s trade routing, Raydium leads with a 26% share, closely followed by SolFi, a private automated market maker (AMM) operating without a front-end interface, holding 18.4%. Orca rounds out the top three with a 13% share.

Jupiter notably excels with its highly diversified portfolio of DEX integrations. Within Jupiter’s trade routing, Raydium leads with a 26% share, closely followed by SolFi, a private automated market maker (AMM) operating without a front-end interface, holding 18.4%. Orca rounds out the top three with a 13% share.

In contrast, other aggregators exhibit less diversity. For instance, OKX heavily relies on Raydium, channeling 66.8% of its volume through this single DEX. Similarly, Titan predominantly favors Orca, which constitutes over 57% of its routed trades. DFlow provides a more balanced distribution, though still dominated by Orca and Raydium, holding 32.1% and 30.6%, respectively.

The Rise of Private AMMs

A distinguishing characteristic of Jupiter, setting it apart from other aggregators, is its extensive support for Private AMMs, which have significantly reshaped the aggregator’s internal dynamics. Collectively, these Private AMMs now account for over 27.1% of Jupiter’s total routed volume.

A distinguishing characteristic of Jupiter, setting it apart from other aggregators, is its extensive support for Private AMMs, which have significantly reshaped the aggregator’s internal dynamics. Collectively, these Private AMMs now account for over 27.1% of Jupiter’s total routed volume.

The surge of Private AMMs has profoundly impacted the dominance of established DEXs like Raydium and Orca. Raydium, once a dominant force with a 40.1% share in October 2024, saw its proportion of volume sharply reduced to less than 11% by May 2025. Similarly, Orca’s share dropped from 17.8% to under 8.1% over the same period.

Conversely, SolFi’s dramatic rise exemplifies the shifting dynamics within Jupiter. Starting from a mere 0.06% share in October 2024, SolFi catapulted to over 35.3% in May, reflecting the aggregator’s strategic pivot towards private, backend-focused liquidity solutions.

The Future Landscape

The sustained growth and evolving market strategies among Solana’s aggregators underscore their central role within the broader decentralized finance landscape. As trading patterns continue to shift, and as new competitors seek market entry, the battle among aggregators is poised to intensify.

Solana’s aggregators, particularly Jupiter, are clearly the quiet powerhouses of this ecosystem, shaping the competitive landscape through strategic partnerships, innovation in liquidity provision, and responsive adjustments to trader demands. The coming months will undoubtedly offer further insights into how these pivotal players adapt to the ever-changing dynamics of decentralized trading.

Stay tuned for further insights into how these platforms evolve and shape the future of DeFi trading on Solana.

This piece is part of our Solana Data Insights series. Make sure to subscribe to Solana Data Insights for weekly onchain analysis.

Read More on SolanaFloor

SEC Says PoS Staking Isn't a Securities Transaction - $SOL Staking ETFs Next?