Взрывной интерес к ДАТ Solana затмевается системными рисками

Казначейские облигации с цифровыми активами могут ускорить прорыв вершины цикла и последующую спираль смерти

- Опубликовано:

- Отредактировано:

Вдохновленные успехом "Стратегии" Майкла Сейлора, инвесторы TradFI безнаказанно создают казначейские облигации цифровых активов (DAT), накачивая зомби-акции и криптовалюты по всем рынкам.

Новые DAT встречаются с безудержным энтузиазмом. Такие лидеры, как Майкл Сейлор и Том Ли, прославляются как пророки будущих прибылей. Инвесторы TradFi не теряют времени даром, выписывая 9-10-значные чеки для реализации стратегий накопления $SOL и запуска маховиков up-only.

Похоже, люди забывают или предпочитают игнорировать тот факт, что маховики не являются самоподдерживающимися. Без внешних сил, подталкивающих к непрерывному движению, паруса начинают топорщиться. Только когда прилив закончится, мы увидим, кто плавает голым.

Представляют ли ДАТ системный риск для Соланы? Как выглядит разгадка ДАТ и какая компания представляет наибольший риск?

Насильственные наслаждения и насильственные концы маховика ДАТ

.ДАТ захватили воображение и внимание криптовалютных рынков. Хотя каждый DAT - это инвестиционный инструмент с множеством нюансов, криптовалютные компании, как правило, используют один и тот же экономический маховик.

-

Компания аккумулирует $SOL

-

Компания’агрессивно накапливает $SOL, что приводит к росту цен

. -

Увеличение цен на $SOL повышает NAV компании&rsquo ;.

-

Компания привлекает больше средств на фоне роста ее оценки

-

Повторение

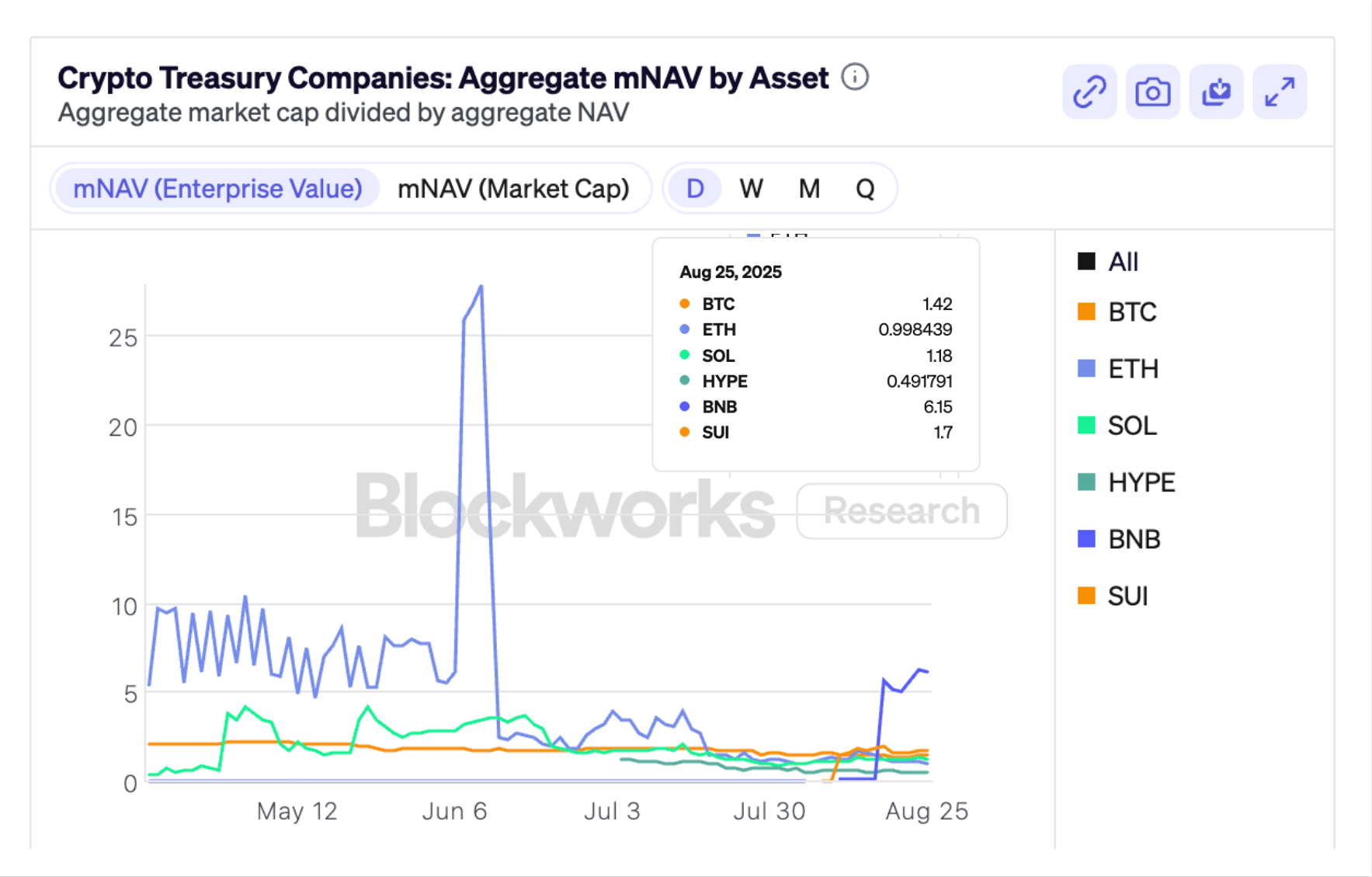

ДАТ обычно полагаются на то, что их акции торгуются с премией к их СЧА, создавая положительную mNAV, которая представляет собой стоимость компании по отношению к ее криптовалютным активам. Если mNAV компании DAT = 2, это означает, что рынок оценил компанию в 2 раза выше стоимости ее криптовалют. Если mNAV больше 1, компания может привлечь средства с помощью различных методов выпуска акций, чтобы купить больше $SOL.

На первый взгляд, DAT выглядит как тонко завуалированная длинная позиция по $SOL с кредитным плечом. Принимая на себя долговые обязательства или выпуская новые акции и разбавляя инвесторов, DAT могут постоянно финансировать текущее накопление $SOL и получать доходность за счет вознаграждения по ставкам.

Все, начиная от соучредителя Solana Labs Раджа Гокала и заканчивая флипперами мемкоинов, высказались в поддержку ‘маховика формирования капитала’, используемого в Solana DATs. Однако новость о том, что заблокированные, уцененные $SOL теперь торгуются с зарождающимися DAT, вызвала новые вопросы об их долговечности и влиянии на рынок.

Перед тем как перейти к более сомнительным обвинениям, давайте&rsquo ; кратко опишем различные точки зрения на ДАТ Solana.

Дело быков

Адвокаты в пользу Solana DATs утверждают, что $SOL занимает уникальную позицию в качестве наилучшего базового актива для криптовалютных казначейских компаний. Генерируя 6-8% годовых за счет вознаграждения за ставку, доходность $SOL’а делает его более привлекательным вариантом, чем биткоин.

Солана, несомненно, является одним из самых привлекательных криптовалютных активов. Сеть может похвастаться большим количеством пользователей, чем любой другой блокчейн, на несколько порядков, и является самой популярной платформой для основателей и разработчиков, создающих новые приложения.

Казначейские облигации с долгосрочными перспективами не подвержены влиянию волатильности mNAV. Если mNAV > 1, это благоприятствует выпуску акций и позволяет DAT привлекать больше средств; когда mNAV падает ниже 1, DAT могут использовать привлеченные средства, чтобы завладеть дешевыми $SOL и увеличить свою долю SOL-per Share.

Solana Defi позволяет ДАТ дополнительно использовать свои активы для увеличения накопления. Например, DAT, выпустившие LST, такие как Defi Development Corporation, могут активно брать кредиты под заложенные $SOL, чтобы покупать больше $SOL.

Цена $SOL напрямую растет по мере того, как все больше DAT сообщают о своих планах по накоплению $SOL в будущем. Каждый раз, когда казначейство объявляет об аппетитном повышении, держатели $SOL могут обоснованно полагать, что компания будет постоянно покупать $SOL и поддерживать рост стоимости актива.

Не слишком ли все это хорошо, чтобы быть правдой?

Медвежий случай

Как бы маховик DAT ни турбировал восхождение $SOL’а, рефлексивная петля обратной связи работает и в обратном направлении. Хотя некоторые могут утверждать, что падение mNAV позволяет DAT накапливать больше $SOL по более низким ценам и увеличивать их $SOL на акцию, негативные ценовые колебания могут оказать опасное влияние на здоровье DAT.

Падающие цены на $SOL будут эффективно размывать СЧА ДАТ&rsquo ;, снижая ее mNAV до уровней, на которых компании может быть трудно привлечь текущий капитал. В зависимости от того, каким образом компании привлекали средства, некоторые DAT могут подвергнуться принудительной продаже, чтобы выполнить требования по долговым обязательствам.

На момент публикации материала 1-3 биткоин-казначейские компании в настоящее время торгуются с mNAV ниже 1, а данные Blockworks свидетельствуют о том, что совокупный mNAV всех $ETH DAT также опустился ниже 1.

Эфирная DAT Sharplink недавно объявила о запуске программы обратного выкупа акций, продемонстрировав, что некоторые DAT решат выкупить акции для поддержания стоимости своих обыкновенных акций. Компания заявила, что обратный выкуп будет способствовать росту стоимости, когда цена акций будет торговаться ниже СЧА. Однако это становится скользкой дорожкой к ликвидации активов для защиты цены акций, особенно в случае компаний, которые выбрали привлечение средств за счет долгов.

Хотя маловероятно, что ДАТ будут продавать свои активы, чтобы защитить падающую цену акций, компании, оказавшиеся в затруднительном положении, могут стать легкой мишенью для инвесторов-активистов и ревностных акционеров.

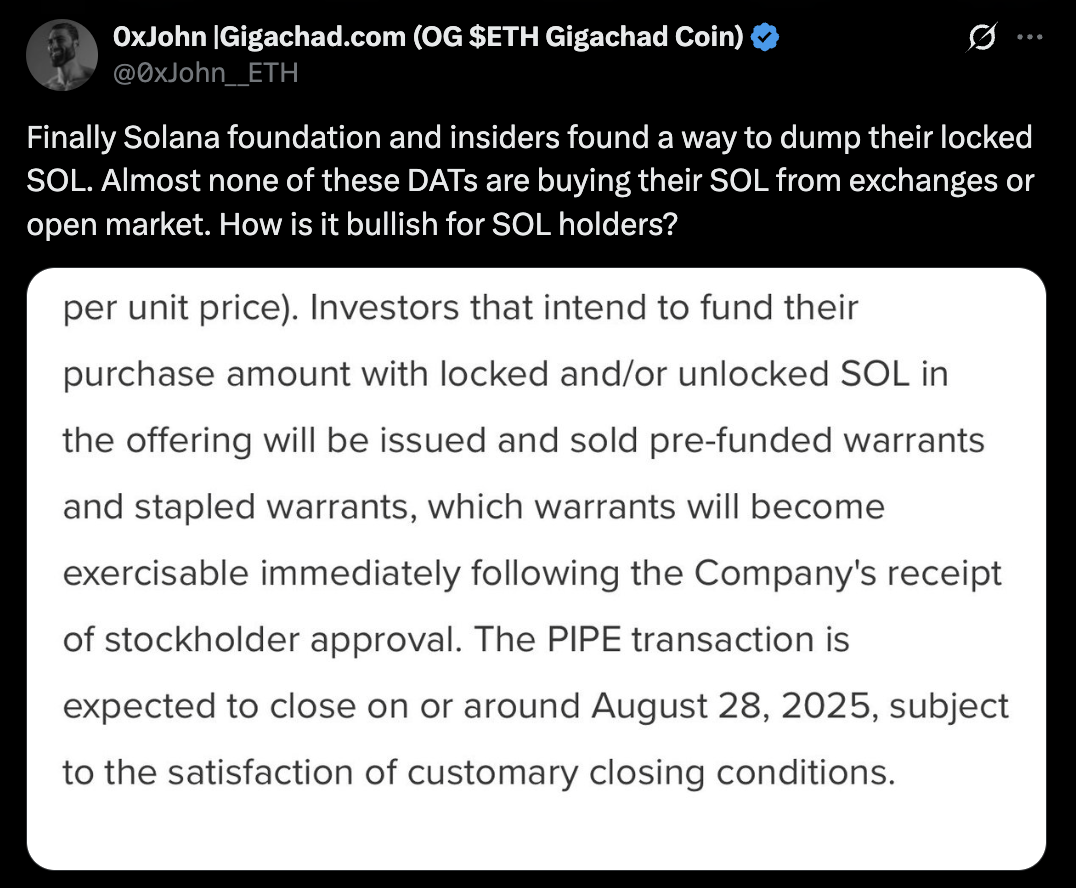

Возможно, ободренный влиянием серийных выступлений Тома Ли за $ETH, Фонд Солана вышел на ринг, чтобы найти защитника Solana&rsquo ; TradFi. По сообщениям, некоммерческая организация подписала письмо о намерениях с Sharps Technology о продаже заблокированных $SOL на сумму $50 млн с 15-процентной скидкой к средневзвешенной по времени цене актива за 30 дней.

Участие фонда в гонке вооружений DAT многие считают бычьей перспективой для цены $SOL в будущем, но некоторые комментаторы утверждают, что это событие попахивает нечестной игрой. Ави Фелман утверждает, что передача заблокированных $SOL казначейским механизмам - это окольный путь, позволяющий таким фондам, как Pantera, “бросить розницу”.

.Обменяв заблокированные $SOL на размещение акций и экспозицию $SOL-via-DAT, фонды могут получить прибыль и выйти из своих позиций, продав обыкновенные акции на публичных рынках.

Другие осудили продажу заблокированных акций $SOL, заявив, что она дает инвесторам и крупным держателям стратегию ускоренного выхода и не окажет никакого влияния на динамику рынка $SOL. 25 августа Bloomberg сообщил, что Galaxy, Multicoin и Jump Crypto участвуют в привлечении $1 млрд для создания новой подтвержденной Фондом Solana DAT.

.Это противоречит опубликованному в конце июля отчету исследователя Galaxy Digital Уилла Оуэнса, который утверждает, что обилие модели DAT сделало маховик “конструктивно хрупким”. Другие предсказывают, что феномен DAT может спровоцировать событие, напоминающее крах GBTC в 2022 году.

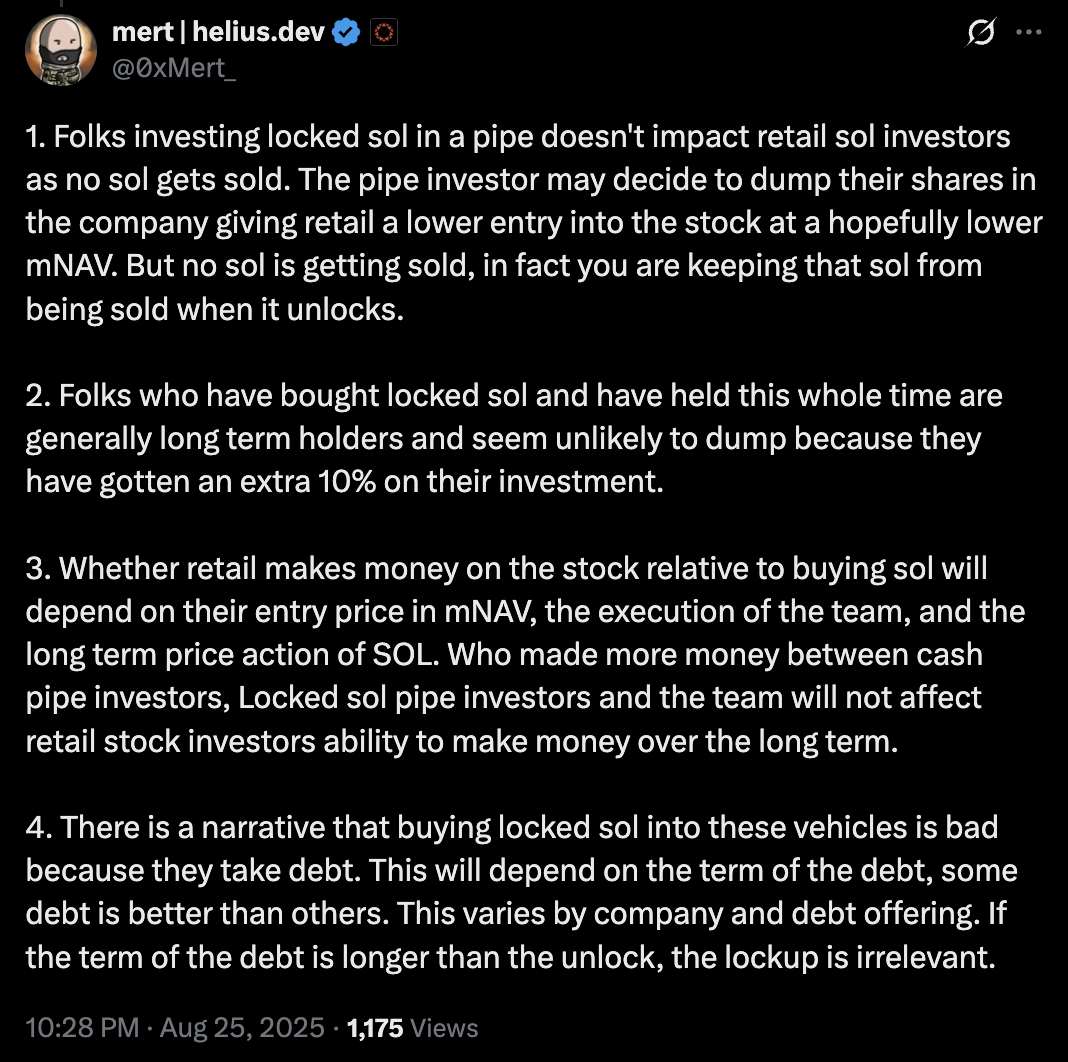

Соучредитель компании Helius Мерт Мумтаз преуменьшил предполагаемый злой умысел, связанный с продажей заблокированных акций $SOL. Отвечая обеспокоенным комментаторам, Мумтаз заявил, что никакие $SOL не продаются и что фонды, покупающие закрытые $SOL, как правило, являются долгосрочными держателями, стремящимися получить более 10 % прибыли от своих инвестиций.

Прежде чем собирать факелы и вилы, стоит отметить, что участие Solana Foundation’в создании DAT меркнет по сравнению с позиционированием его конкурентов из Ethereum Foundation. EF продала 10 000 $ETH компании Sharplink в рамках внебиржевой сделки в июле 2025 года, во многом благодаря тесной связи с председателем совета директоров Sharplink Джозефом Лубиным, соучредителем Ethereum и нынешним генеральным директором R&D фирмы Consensys.

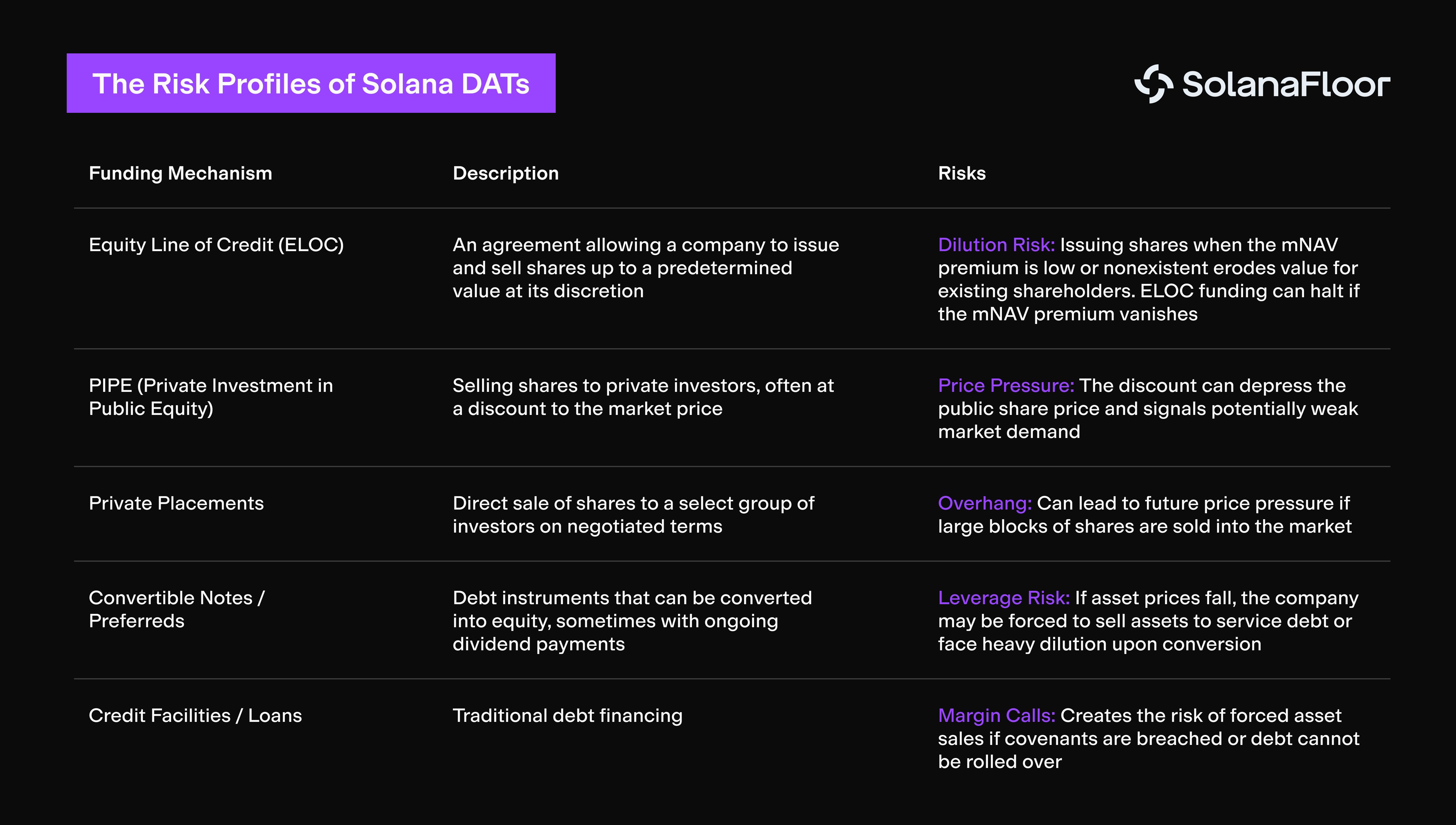

Профили риска DAT от Solana

ДАТы Solana’использовали различные стратегии для привлечения миллиардов якобы незадействованного капитала, который только и ждет, чтобы быть использованным на криптовалютных рынках.

Соланы DAT, занимающие долговые позиции, например, кредитные линии, подобные тем, что открыла Sol Strategies в январе 2025 года, представляют системный риск. В случае если курс $SOL опустится ниже ликвидационной цены Sol Strategies, холдинговая компания может быть вынуждена продать свой пакет акций, чтобы выполнить долговые обязательства.

Другие казначейские компании на базе Solana, продемонстрировавшие готовность взять на себя более высокий уровень риска, включают Classover Holdings и лидера рынка Upexi. Кредитная линия Classover’$500 млн состоит из старших обеспеченных конвертируемых облигаций. Эти облигации обеспечены "первоочередным защищенным залоговым правом на все существующие и будущие активы компании", что явно включает криптовалюту, купленную на полученные средства. В случае дефолта кредиторы могут арестовать и ликвидировать казначейство компании SOL.

Это приводит нас к Upexi. Имея более 200 млн долларов СОЛ, крупнейшая компания Solana’DAT воспользовалась различными стратегиями финансирования, включая PIPE-привлечение и 150 млн долларов обеспеченного конвертируемого векселя обеспеченного спотом и заблокированного СОЛ, который представляет угрозу ликвидации и может быть арестован кредиторами в случае спада на рынке.

Как выглядит разворачивающийся DAT?Ликвидация - опасная игра на любом уровне сложности. При всем своем опыте и знаниях операторы DAT ’не так уж сильно отличаются от преступников-дегенератов, желающих получить все обратно за одну сделку.

После объявления о многочисленных 9-10-значных сборах средств на покупку $SOL, DAT были приняты криптосообществом с распростертыми объятиями. Однако распространение этой инвестиционной модели и ‘маховик капиталообразования’, который она поддерживает, представляют собой системный риск, который нельзя игнорировать.

ДАТ, основанные на долгах, представляют наибольшую угрозу для существующих держателей $SOL. Если динамика цен на $SOL приведет к тому, что криптовалютные казначейства опустятся до уровня ликвидации, вынужденная продажа активов стоимостью в миллионы долларов может привести к порочной спирали смерти. Это приведет к тому, что более устойчивые DAT окажутся на опасной территории с резко сниженными mNAV.

Подводные казначейские компании окажутся без желающих LP и инвесторов. Не желающие нести убытки акционеры могут вынудить DAT ликвидировать свои пакеты акций, чтобы сохранить капитал, что приведет к дальнейшему падению рынка.

Остается нерешенным вопрос: волнует ли это криптовалютный рынок? Финансовые рынки неумолимы по своей природе, но криптовалютный ’культурный зейтгейст" прославил такие термины, как “no crying in the casino”.

Некоторые из самых ярых сторонников криптовалют с удовольствием отмечают, что появление DAT - это не более чем ироничная пирамида, с помощью которой TradFi обеспечивает своевременную ликвидность для выхода криптовалютных аборигенов. Почему нас должно волновать, что акционеры будут разбавлены, если это накачает наши сумки, или что LP вложит средства в обмен на обыкновенные акции, которые потеряют в цене?

Играйте в глупые игры, выигрывайте глупые призы. Зачем подвергать сомнению несовершенную систему, если вы можете извлечь из нее выгоду?

В глазах игроков с большими деньгами криптовалютные DAT являются вырожденным кузеном менее гламурных криптовалютных ETF и, несомненно, самой захватывающей вещью, которая произойдет в этом цикле. Маховик высоких ставок является искусным прикрытием для миллиардной игры в музыкальные стулья, которая может стать катализатором этого раунда и начала следующей крипто-зимы.

Читать подробнее о SolanaFloorTradFi нацелилась на Solana BTC-Fi

Zeus Network будет обеспечивать поиск доходности биткоина на Solana на бирже NASDAQ Metalpha’

Компания TradFi нацелилась на Solana BTC-Fi.

У Solana проблемы с восприятием?