Assessing Marinade’s $MNDE Buyback Plan: Revenue, Deflation, and DAO Strategy

Projected Annual Deflation Rate: 4.9% of Total $MNDE Supply

- Published:

- Edited:

Marinade is planning a strategic adjustment to its own token economics. The latest proposal, MIP.11, aims to redirect 40% of SAM performance fees—previously held in the DAO treasury—toward buying back $MNDE tokens from the open market. If passed, this move would not only reduce $MNDE’s circulating supply but also reinstate long-awaited utility for holders.

The decision is now in the hands of the community and will be finalized through an on-chain market vote managed by MetaDAO.

Why This Matters: SAM Revenue and Its Growing Role

Marinade has emerged as one of the most innovative staking protocols on Solana, thanks in large part to its Stake Auction Marketplace (SAM). SAM allows validators to bid for stake in exchange for higher yields to stakers, helping to optimize capital efficiency while generating substantial protocol revenue.

Revenue sources for Marinade include $SOL inflation, MEV (Maximal Extractable Value), and fees from SAM. While 90.5% of that income is funneled back to stakers, 9.5% flows into the DAO Treasury—funds that are now being proposed for partial redirection into $MNDE buybacks.

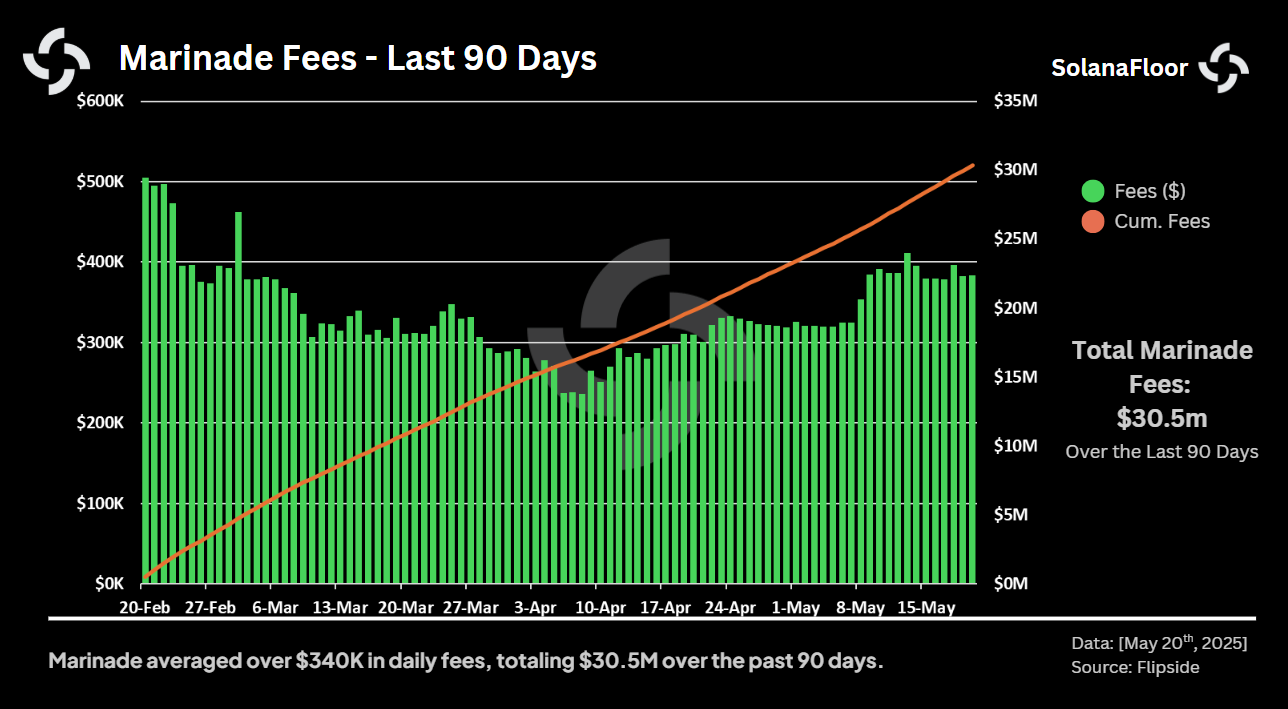

According to Flipside data, Marinade has generated over $30.5 million in fees over the past 90 days. More recently, average daily fees have hovered around $380,000, with occasional peaks exceeding $411,000 on days of heightened Solana activity. Even during low-traffic periods, daily fees rarely dropped below $250,000—a testament to the robustness of Marinade’s revenue streams.

According to Flipside data, Marinade has generated over $30.5 million in fees over the past 90 days. More recently, average daily fees have hovered around $380,000, with occasional peaks exceeding $411,000 on days of heightened Solana activity. Even during low-traffic periods, daily fees rarely dropped below $250,000—a testament to the robustness of Marinade’s revenue streams.

Buybacks, Deflation, and Token Utility

Under MIP.11, 40% of the DAO’s share of these earnings—equivalent to 3.8% of total protocol revenue—would be allocated to $MNDE buybacks.

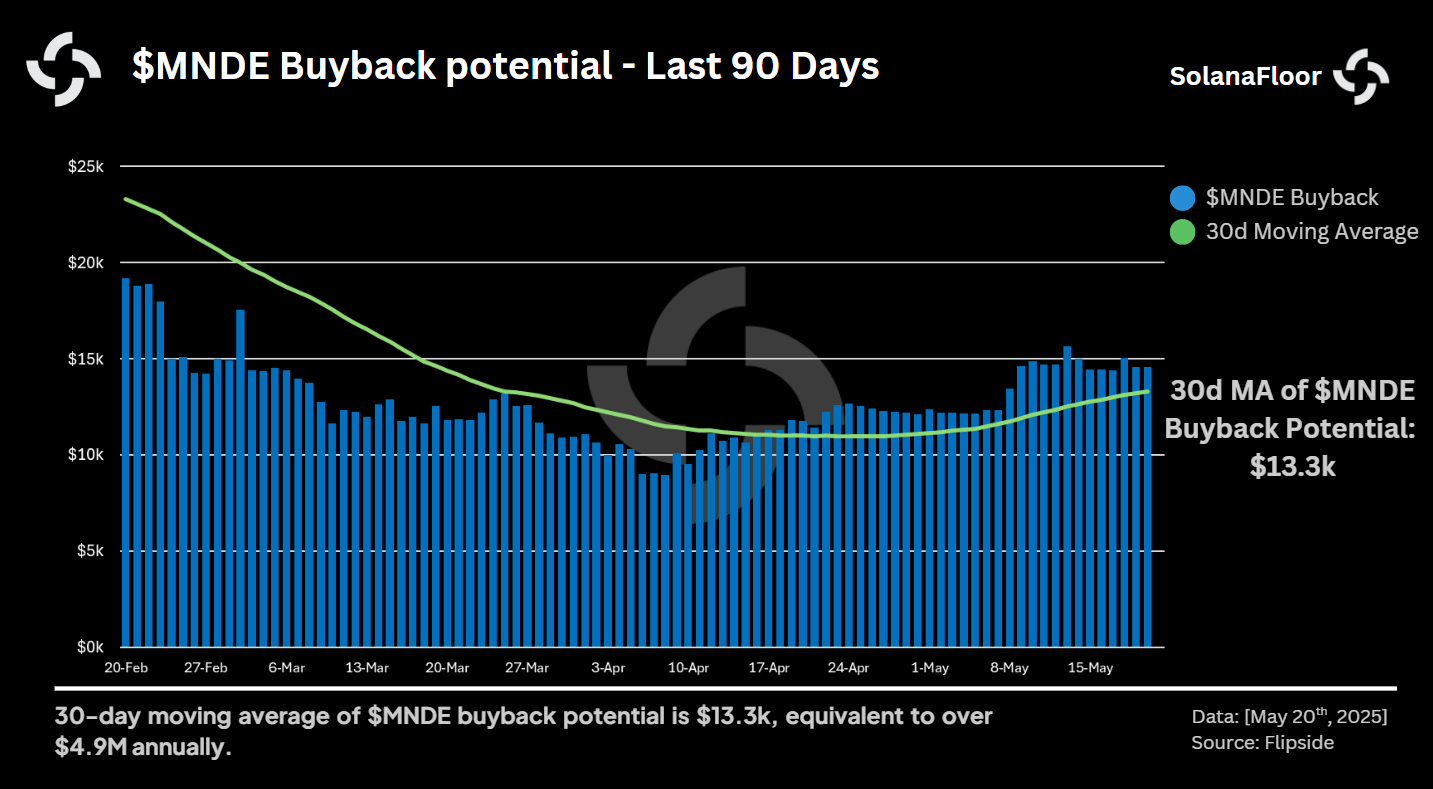

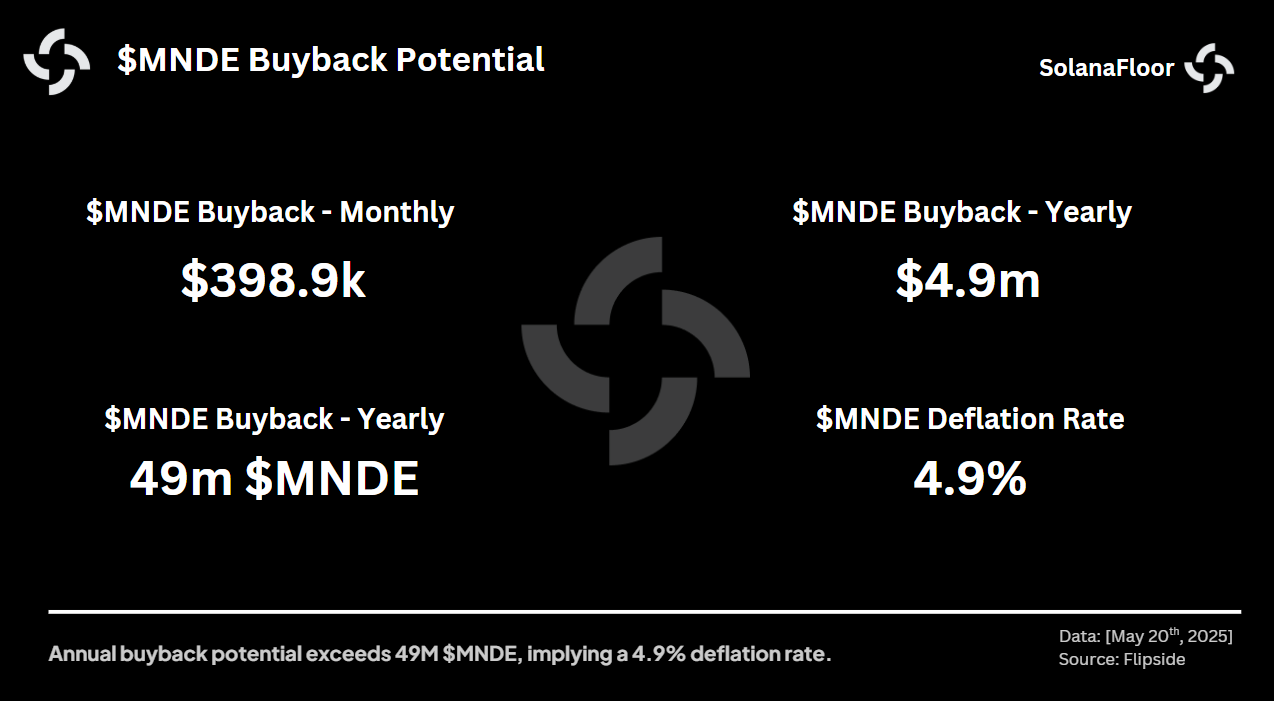

Crunching the numbers reveals that the $MNDE buyback potential over the last three months has ranged from $9,000 to $19,000 per day, with a 30-day moving average of approximately $13,300. On a monthly basis, that translates to about $398,900, and on an annual scale, a staggering $4.9 million.

Crunching the numbers reveals that the $MNDE buyback potential over the last three months has ranged from $9,000 to $19,000 per day, with a 30-day moving average of approximately $13,300. On a monthly basis, that translates to about $398,900, and on an annual scale, a staggering $4.9 million.

At current $MNDE prices, this level of buyback activity would remove over 49 million $MNDE tokens from circulation annually. Given that the total supply stands at 1 billion, the proposal introduces an effective 4.9% annual deflation rate—a significant lever to strengthen the token’s price floor and utility narrative.

At current $MNDE prices, this level of buyback activity would remove over 49 million $MNDE tokens from circulation annually. Given that the total supply stands at 1 billion, the proposal introduces an effective 4.9% annual deflation rate—a significant lever to strengthen the token’s price floor and utility narrative.

How Does This Compare to Jito’s $JTO?

The proposal draws inevitable comparisons to Jito, Marinade’s primary rival in the Solana staking space. Not long ago, Jito announced its own buyback initiative for its native token, $JTO, which generated buzz for its bold deflationary stance.

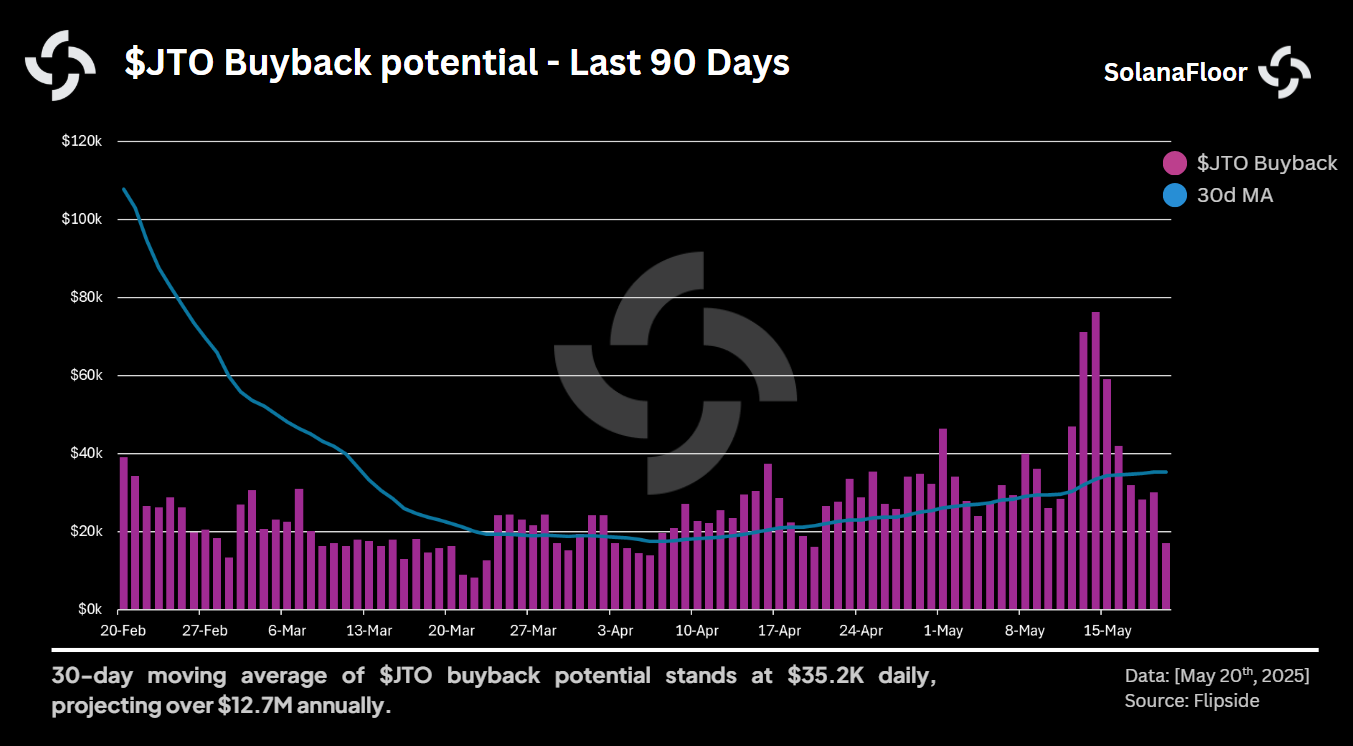

According to our prior analysis, Jito’s buyback program can retire about 11 million $JTO per year, producing an estimated 1.1 % annual deflation rate. Under MIP-11, the projected impact for $MNDE is much larger—up to 49 million tokens removed annually, or roughly 4.9 % of the supply.

According to our prior analysis, Jito’s buyback program can retire about 11 million $JTO per year, producing an estimated 1.1 % annual deflation rate. Under MIP-11, the projected impact for $MNDE is much larger—up to 49 million tokens removed annually, or roughly 4.9 % of the supply.

The wide gap is partly explained by $MNDE’s lower market capitalization relative to $JTO; the same dollar amount of buybacks retires a larger share of $MNDE’s supply. Of course, the ultimate deflation rate for either token will still hinge on variables such as token price, revenue consistency, and how fully each proposal is executed.

Final Thoughts: A Turning Point for Marinade?

Marinade’s proposal represents a shift in how DeFi protocols on Solana are thinking about token utility and treasury strategy. Redirecting a portion of protocol earnings toward token buybacks is one method for attempting to balance long-term sustainability with community expectations.

Still, questions remain. How consistent will protocol revenue be over time? Will this mechanism provide meaningful support to MNDE’s value or engagement metrics? And how will it affect other areas of the DAO's budgeting priorities?

As with many proposals in decentralized governance, the outcome will depend on execution and evolving network dynamics. MIP.11 may offer a new model for value alignment—or simply serve as one of many experiments in the ongoing development of staking protocols on Solana.

Read More on SolanaFloor: