Jupiter Reclaims Dominance with 93.6% Market Share in Solana’s Aggregator Landscape

Aggregator competition is increasingly defined by routing design, execution quality, and liquidity sourcing.

- 公開:

- 編集済み:

Over the past year, Solana’s decentralized exchange (DEX) ecosystem has undergone a quiet but meaningful structural shift. While attention has often focused on new tokens, memecoin cycles, or the growth of perpetual futures, a more foundational change has been unfolding beneath the surface: the rapid consolidation of DEX flow through aggregators and the increasing importance of routing logic and execution quality.

For several months, market participants speculated that Jupiter’s near-monopoly position among Solana-based aggregators could be challenged. Comparisons were frequently drawn to the perpetual trading market, where the launch of Pacifica introduced credible competition and redistributed market share. New entrants such as Titan, alongside the rise of DFlow and other routing solutions, were widely expected to erode Jupiter’s dominance. Onchain data, however, tells a more nuanced story.

A Temporary Erosion of Market Share

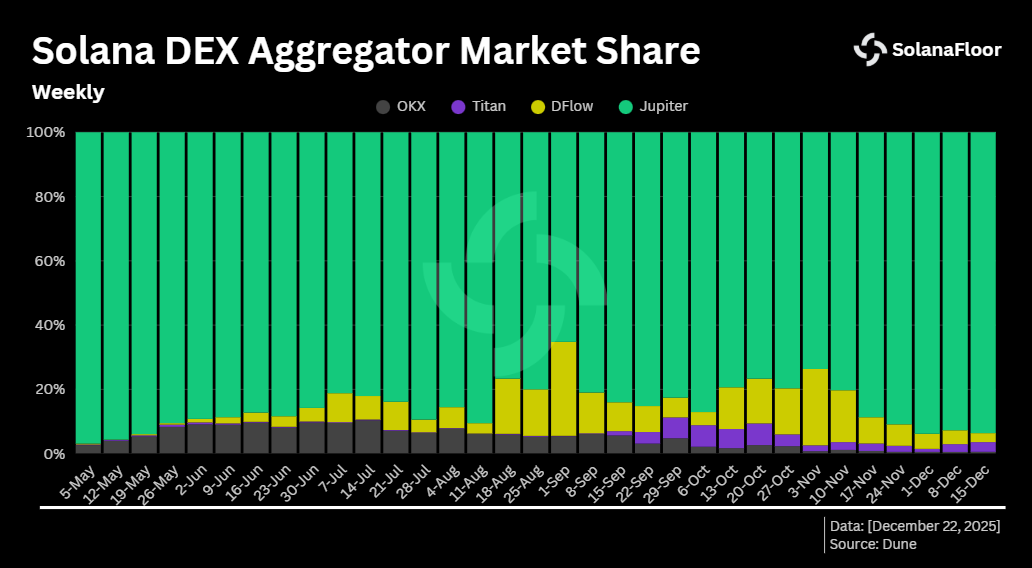

According to Dune Analytics, Jupiter’s share of Solana aggregator volume began to decline in early May, coinciding with a broader rise in weekly DEX trading routed through platforms such as DFlow and OKX. Jupiter’s dominance fell from 96.9% to a local low of 65.2% during the first week of September. At the same time, DFlow reached its own peak market share of 29.2%.

According to Dune Analytics, Jupiter’s share of Solana aggregator volume began to decline in early May, coinciding with a broader rise in weekly DEX trading routed through platforms such as DFlow and OKX. Jupiter’s dominance fell from 96.9% to a local low of 65.2% during the first week of September. At the same time, DFlow reached its own peak market share of 29.2%.

Despite this drawdown, Jupiter never lost majority control on a weekly basis. Other aggregators were unable to collectively push Jupiter’s share below the 50% threshold, underscoring the depth of its integration across Solana’s liquidity venues.

On a daily timeframe, the competitive pressure briefly intensified. On November 15, DFlow captured 47.9% of aggregator-driven DEX volume, narrowly overtaking Jupiter, which fell to 47.1%. This marked the first instance in which Jupiter ceded the top position, even if only for a single day. The reversal was short-lived. In the weeks that followed, Jupiter reasserted its dominance, climbing back above 90% market share and reaching over 93.6% in the most recent week, its highest level in roughly six months.

Solana-Only, Yet Growing Faster

Jupiter’s resurgence is particularly notable given its Solana-exclusive focus. Unlike several competitors that operate across multiple blockchains, Jupiter’s activity is confined to a single ecosystem. Even so, its relative growth has outpaced that of multi-chain aggregators.

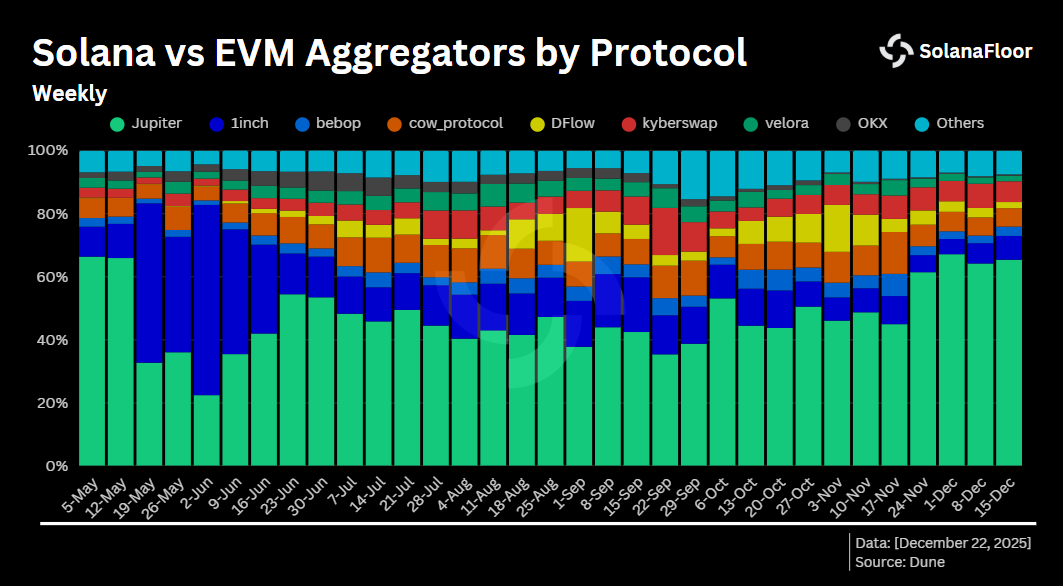

During the week of November 24, Jupiter’s share of global aggregator volume rose sharply from 44.9% to over 61.4%, before extending to 65.4% in the following week. By contrast, 1inch, long regarded as one of the dominant aggregators across EVM-compatible chains, has seen its market share contract significantly. After peaking above 60% in early June, 1inch now accounts for just 7.5% of total aggregator volume. In practical terms, Jupiter has emerged as the largest aggregator by volume, despite operating on only one chain.

During the week of November 24, Jupiter’s share of global aggregator volume rose sharply from 44.9% to over 61.4%, before extending to 65.4% in the following week. By contrast, 1inch, long regarded as one of the dominant aggregators across EVM-compatible chains, has seen its market share contract significantly. After peaking above 60% in early June, 1inch now accounts for just 7.5% of total aggregator volume. In practical terms, Jupiter has emerged as the largest aggregator by volume, despite operating on only one chain.

Aggregators Absorbing DEX Flow

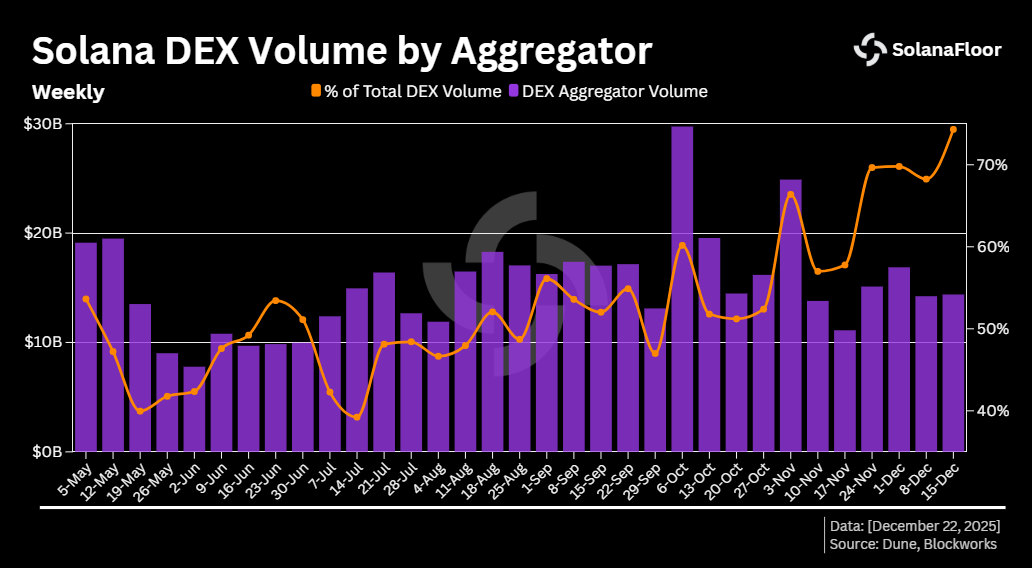

This shift is occurring alongside a broader trend, an increasing proportion of Solana DEX volume is now routed through aggregators rather than executed directly on individual venues. Over the past six months, the weekly share of DEX trades executed via aggregators has climbed from roughly 40% to over 74.3%, marking the highest level observed during this period.

This shift is occurring alongside a broader trend, an increasing proportion of Solana DEX volume is now routed through aggregators rather than executed directly on individual venues. Over the past six months, the weekly share of DEX trades executed via aggregators has climbed from roughly 40% to over 74.3%, marking the highest level observed during this period.

Growth has accelerated in recent months. Aggregator share has expanded by approximately 1.7× over the past three months alone and increased by more than 6% in the most recent week. The peak weekly volume captured by aggregators occurred during the week of October 6, when routed DEX volume exceeded $29.7B. These figures suggest that aggregators are no longer a peripheral convenience layer, but a primary interface through which liquidity is accessed on Solana.

Prop-AMMs and the Rise of Cyclic Arbitrage

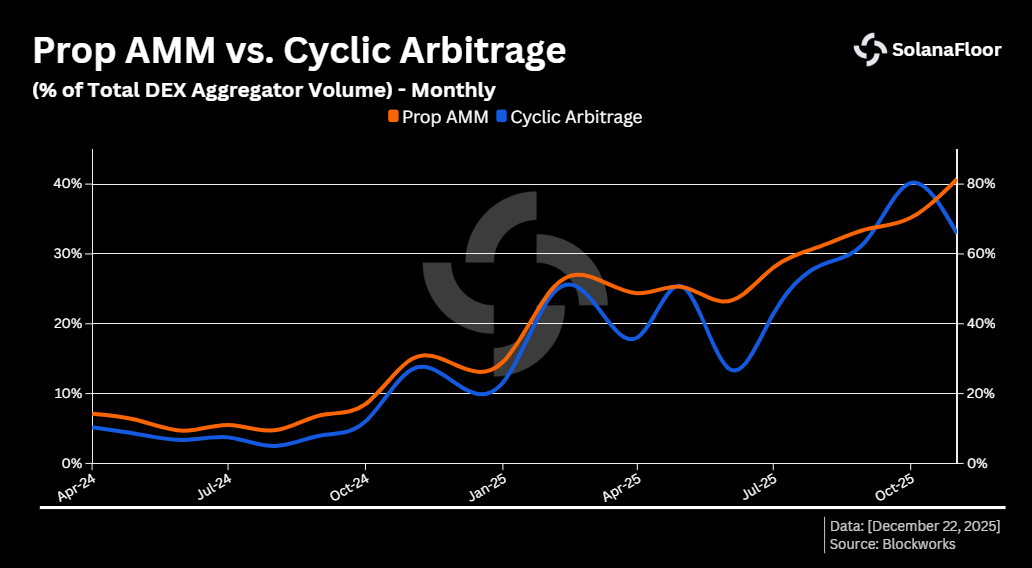

One of the more consequential developments within this aggregator-driven flow has been the emergence of proprietary automated market makers (Prop-AMMs). Since early 2025, the surge in cyclic arbitrage has largely been the result of increasing activity across Prop-AMMs, as their growing share of routed volume has introduced more dynamic pricing and exploitable inefficiencies.

In August 2024, cyclic arbitrage accounted for just 2.5% of aggregator-executed DEX volume. By October 2025, that figure had risen above 40%. Over the same period, Prop-AMMs expanded to represent more than 81.3% of total aggregator volume. Prop-AMMs introduce dynamic, highly responsive pricing models that create short-lived inefficiencies across fragmented liquidity pools, making cyclic arbitrage both viable and increasingly prevalent.

In August 2024, cyclic arbitrage accounted for just 2.5% of aggregator-executed DEX volume. By October 2025, that figure had risen above 40%. Over the same period, Prop-AMMs expanded to represent more than 81.3% of total aggregator volume. Prop-AMMs introduce dynamic, highly responsive pricing models that create short-lived inefficiencies across fragmented liquidity pools, making cyclic arbitrage both viable and increasingly prevalent.

Liquidity Concentration Across Aggregators

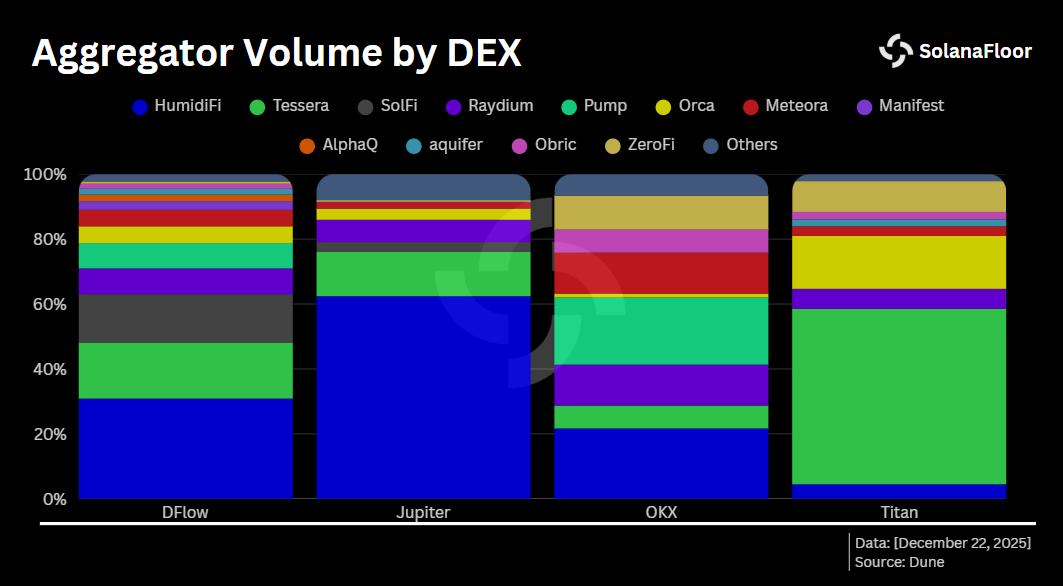

Today, Prop-AMMs dominate execution across all major Solana aggregators, though their internal composition varies. On Jupiter, HumidiFi alone accounts for over 62.4% of executed volume, with total Prop-AMM share exceeding 79.5%. DFlow shows a more distributed structure: HumidiFi leads with 30.8%, followed by Tessera at 17.29% and SolFi at 14.89%.

Today, Prop-AMMs dominate execution across all major Solana aggregators, though their internal composition varies. On Jupiter, HumidiFi alone accounts for over 62.4% of executed volume, with total Prop-AMM share exceeding 79.5%. DFlow shows a more distributed structure: HumidiFi leads with 30.8%, followed by Tessera at 17.29% and SolFi at 14.89%.

Titan presents a contrasting profile. Unlike its peers, Tessera represents the majority of Titan’s volume, accounting for more than 54%, while Orca ranks second with 16.3%.

A Maturing Execution Layer

Taken together, these trends point toward a maturing execution layer on Solana. Aggregators have consolidated their role as the dominant access point for DEX liquidity, Jupiter has reaffirmed its central position after a period of competitive pressure, and Prop-AMMs have reshaped how price discovery and arbitrage function at scale.

Rather than fragmenting Solana’s trading landscape, competition among aggregators appears to be reinforcing a more efficient, albeit increasingly concentrated, market structure, one where execution quality, routing sophistication, and liquidity design matter more than ever.

This piece is part of our Solana Data Insights series. Make sure to subscribe to Solana Data Insights for weekly onchain analysis.

Read More on SolanaFloor

Privacy Cash: Over $121M in Private Transfers During Its First 100 Days

Matt Hougan: BSOL Leads, Solana Adoption Just Hit a Turning Point, Here's What's Next!